|

Financial Professionals Fall 2021

This is my quarterly missive intended primarily for my fellow financial professionals wherein I share items I have run across or thought about this quarter which I think might be beneficial to you. Enjoy!

We occasionally take consulting clients (typically RIA firms). The annual retainer for this is generally the square-root of your AUM (with a minimum of $10,000 and maximum of $50,000). For more details or to discuss further, please e-mail or call me at 770-517-8160. – David

First, Taleb (author of The Black Swan, Fooled by Randomness, Antifragile, etc.) has a paper out on Bitcoin, Currencies, and Fragility.

In other crypto news, a paper from folks from MIT and State Street is out. Money quote:

[A] lottery preference for returns above 20% supports some exposure to cryptocurrencies even if they are not expected to generate a positive return. Without a lottery preference, however, investors require cryptocurrencies to return at least 30% to support an allocation to them.

In other words, if you aren’t gambling, you would need an expected return of 30% on crypto to justify a 1% weight in the portfolio (table on page 21).

Second, many people who haven’t adequately prepared for retirement (financially) plan to just “work longer” (I’ve even heard “until I die”). But that frequently isn’t controllable. Here is a paper with some data. Most relevant, even in the best cases (more educated white women), folks who can work at 62 have a 13% chance of not being able to work at 70. In the worst case (less educated black men) it’s a 76% chance of not being able to work at 70. A better approach would be live on half!

Third, I read two research papers from DFA folks that won’t get much press because they don’t have any sensational findings. But null results are still valuable results.

How to rebalance a portfolio (here): there’s no significant impact to returns regardless of methodology, tracking error and turnover offset (if you have more of one, you have less of the other).

How to hedge inflation (here): nothing really does very well (other than TIPS).

Fourth, good papers from Northern Trust on Delaware and Nevada trusts in particular, but very good overview in general:

Delaware Trusts

Nevada Trusts

Also, Florida has updated their trusts with some favorable features, see this.

Fifth, from Daniel Gottlieb and Kent Smetters’ Lapse-Based_Insurance paper:

Most individual life insurance policies lapse, with lapsers cross-subsidizing non-lapsers. We show that policies and lapse patterns predicted by standard rational expectations models are the opposite of those observed empirically. We propose two behavioral models consistent with the evidence: (i) consumers forget to pay premiums and (ii) consumers understate future liquidity needs. We conduct two surveys with a large insurer. New buyers believe that their own lapse probabilities are small compared to the insurer’s actual experience. For recent lapsers, forgetfulness accounts for 37.8 percent of lapses while unexpected liquidity accounts for 15.4 percent.

(I’ve been a guest on Kent’s “Your Money” on SiriusXM Radio.)

Sixth, a good article on some types of permanent life insurance: Explaining Whole Life vs. Guaranteed Universal Life Insurance.

Seventh, I’m sure you have seen headlines about inflation being up over 5% year-over-year (5.2% August 2021 over August 2020). But the year ago numbers were “off” as we were in the middle of a lockdown, so I was curious what the two-year number was as a better measure of how we are “really” doing on inflation. The inflation rate for that previous period was 1.3% (August 2020 vs. August 2019). The two year average then is just 3.2%. That is above the fed’s 2% target, but certainly not extreme – so far anyway. (The math: 1.0132*1.0520)^(1/2)-1=3.2% and FRED data is here.)

In that graph you can see a little upward blip in July of 2008 also. Going from that high to the recent high is an annualized inflation rate of 1.7% over the past 13+ years.

Eighth, great article on “the bezzle” with stuff from Galbraith, Munger, Minsky, etc. here.

Ninth, good piece from GMO on the Value vs. Growth debate here.

Tenth, the idiocy of our politicians always astonishes me:

SSA on August 31, 2021: “Medicare Part A will run out of money in five years.”

Congressional Democrats four days later: “I’ve got it – let’s add 23 million people to the program.”

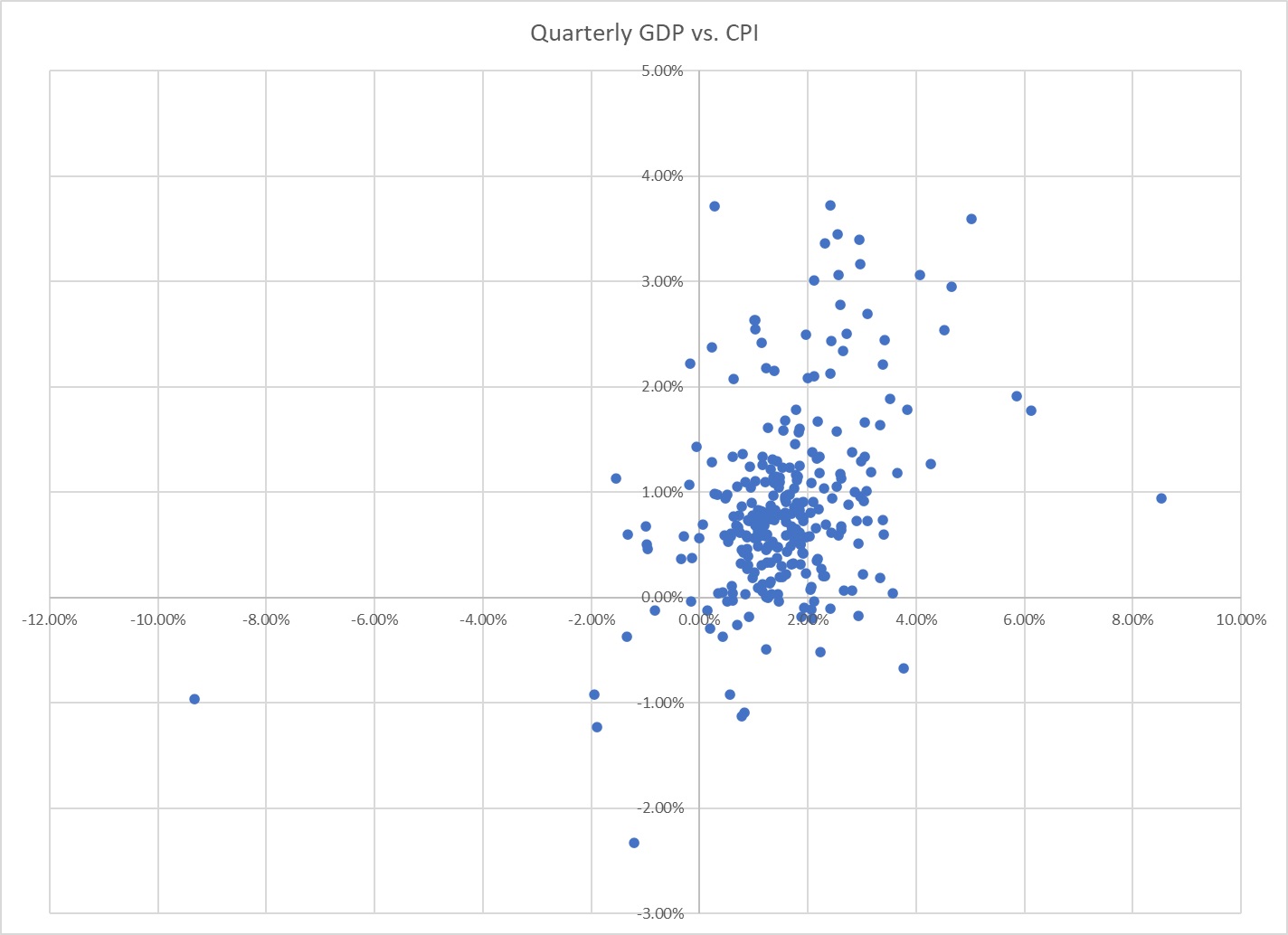

Eleventh, the two things that affect stock and bonds the most are unexpected changes in GDP (mostly stocks) and CPI (mostly bonds). I did a scatter chart in Excel using the FRED data (CPI & GDP) of the quarterly data:

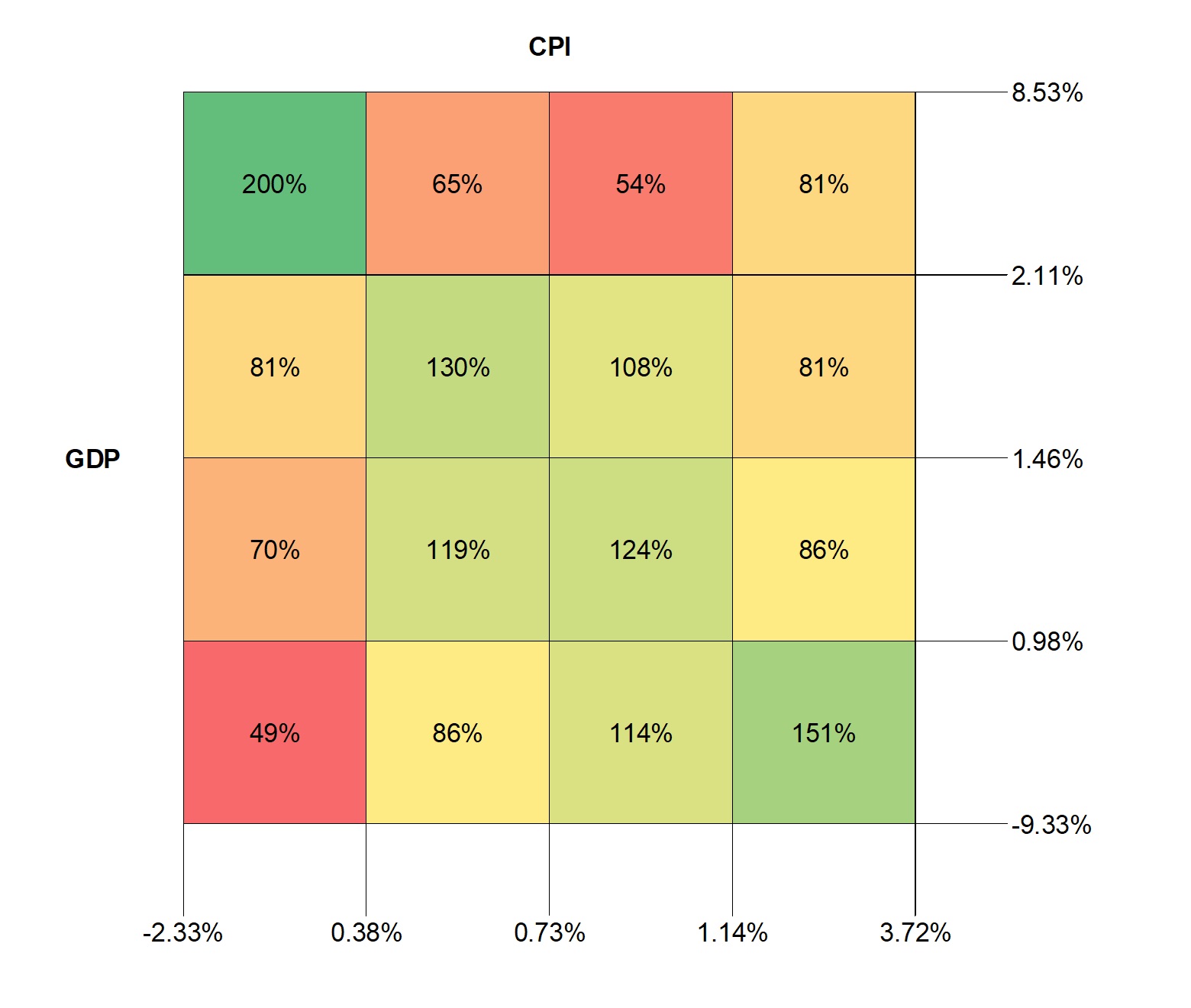

CPI is on the x-axis and GDP (nominal) on the y-axis. It looks like a positive relationship, but I wanted to dig further. I looked at the 25th percentile, the median, and the 75th percentile and divided each (CPI and GDP) separately. So by construction, there are exactly 25% in each section of each metric. Here are the breakpoints (not annualized, this is quarterly data):

|

GDP |

CPI |

Max |

8.53% |

3.72% |

25% |

2.11% |

1.14% |

Median |

1.46% |

0.73% |

75% |

0.98% |

0.38% |

Min |

-9.33% |

-2.33% |

So, if I combine those into a 4x4 grid, and the two are completely independent, then there should be roughly (because of randomness) 1/16 (6.25%) in each box.

Here is what we have. The numbers in the cells show the percentage of what would be expected (i.e. every cell “should” be 100%). As you can see there is a little bit of a relationship running from top left (high GDP and low CPI) to bottom right (low GDP and high CPI):

Now, this doesn’t give us a trading strategy as only unexpected inflation or GDP growth should affect asset prices. Still, I wanted to see what the data looked like. There are fewer low growth and low inflation periods (bottom left) than I would have expected. That might be different if we had more data. This data is from 1947-2020 so it doesn’t include the Great Depression.

Twelfth, what appears to be great analysis of the weight you should give immediate annuities in your portfolio is here. I never thought of it that way before.

What she is saying (which is obvious in hindsight) is that if your spending rate is higher than the sustainable withdrawal rate of the portfolio, but less than the payout rate on an immediate annuity, then you should do a weighted average to get to your number.

But…

The problem is that the SWR is real (inflation adjusted), but the annuity payment isn’t. If you used an inflation-indexed annuity, it would be perfect. But my guess is that the inflation-indexed annuity payout is less than the SWR you would use anyway so it wouldn’t work. The solution is spend less!

Thirteenth, Meb Faber was on a Morningstar podcast: To Be a Good Investor, You Have to Be a Good Loser

Fourteenth, a few more good quotes for you:

It is the mark of an educated mind to be able to entertain a thought without accepting it. – Aristotle

A person who won’t read has no advantage over one who can’t read. – Mark Twain

Fifteenth, I have been interested in equal-weight portfolios for some time and some good research came out on that topic here.

Sixteenth, you have undoubtedly already seen good summaries of the Ways and Means tax proposal, and our associate Kaitlyn wrote up a nice synopsis for us:

- Increase in Corporate Tax Rate (currently: 21%)

- 18% on first $400k

- 21% up to $5 million

- 26.5% thereafter

- Increase in Top Marginal Individual Tax Rate – To 39.6%

- Married w/ taxable income over $450k

- HH w/ taxable income over $425k

- Single w/ taxable income over $400k

- MFS w/ taxable income over $225k

- Estates and Trust w/ taxable income over $12,500

- Increase in Capital Gains Rate – From 20% to 25%

- Surcharge on high Income Individuals, Trusts, and Estates

- Impose a tax equal to 3% of MAGI in excess of $5 million

- QBI: Max. allowable deduction at $500k for MFJ, $400k for Single, $250k for MFS, and $10k for Trust or Estate.

- Revert unified credit against estate and gift taxes to $5 million (adjusted for inflation)

- Prohibit further contributions to IRA or Roth if total value of IRA and defined contribution account exceeds $10 million

- Eliminate Roth conversions for single taxpayers with taxable income over $400k, MFJ with $450k, HH with $425k and all conversions of basis

- RMDs: individual with IRA, Roth IRA, and DC plans with balances exceeding $10 million will require an RMD of 50% of the amount that exceeded $10 million and 100% over $20 million

- End employer credit for wages paid during family and medical leave after 2023 (instead of current expiration of 2025)

- Include grantor trust in taxable estate

- Sales between grantor trust and their deemed owner is equivalent to sales between owner and third party

Seventeenth, I spent a few days in Chicago at a conference and then just reading and thinking. Here are some things of possible interest to you.

First we have lots from Steve Siegel:

- Two SLAT provisions for lawyers to add to prevent a divorce from messing up the plan (though the possible change in grantor trust taxation may torpedo SLATs for many people anyway):

- Require the beneficiary to be the current spouse of the grantor.

- Have a trust protector who can change the beneficiary to any descendant of the grantor’s grandparents. (This would include the grantor!)

- To get a step-up without risk: Gift appreciated property to grandma (or whoever is going to die soon and will leave it back to you) and amend her will to read:

- If I live > 1 year from date of gift property goes to grantor

- If I live < 1 year from date of gift property goes to grantor’s children

- Use testamentary CLATs given the low 7520 rate used in the calculations to avoid estate taxes and give to charity.

A few things from David York:

- Clients need protection against the “four d’s”: Death, Divorce, Disability, and Democrats. (That is my version, his had the “Democrats” crack, which I liked, but I think his other ones were slightly different)

- Attorneys think they are architects but they are really general contractors. You need clarity of purpose before documents. (Again, my paraphrase, but his was very close to that I think.)

Other random things:

- Be a good ancestor. (I didn’t note who said it at the conference, but I’ve heard it before so it isn’t original. I still like it.)

I have a few other things that I was thinking about on my trip:

- I think the business value of a low-quality advisor has high beta and a high-quality advisor has low beta. This is because not only is the low-quality (high-quality) advisor’s portfolios typically more aggressive (conservative), but the advisor attracts more clients in times of euphoria (panic). This isn’t saying anything at all about the respective growth rate of the practice, this is just about the beta of the practice value to the market.

- Can you think of income taxes on a portfolio as options positions? I’m just going to riff on this:

Imagine I have 1,000 shares of stock with a price of $20/share; a basis of $4/share; and a marginal tax rate (now and forever) of 25% (just for simplicity).

I can think of that as a combination of:

- A stock position worth 1,000 * $20 = $20,000

- A liability of ($20 - $4) * 1,000 * 25% = $4,000. This is the tax I owe at-the-money.

- A short ATM call option on 25% of the position. So I have essentially sold a call option on 250 shares with a strike price of $20 and an expiration of whenever I think I will sell (or death, given a step-up). This is the additional taxes I owe if the stock goes up.

- A long ATM put option on 25% of the position. So I have essentially bought a put option on 250 shares with a strike price of $20 and an expiration of whenever I think I will sell (or death, given a step-up). This is the taxes I save if the stock declines. (And if it goes below the basis, I assume I can use the loss against another gain elsewhere.)

That description above is sort of a collar on 250 shares of stock. A collar has treasury equivalent value. In other words, a collar with the positions all at the money, would be a short call plus a long put, plus the stock which equals a treasury. Plugging in the previous values, I can create a treasury by using 25% of the stock (250 shares), plus ATM short calls on 250 shares, plus a long ATM puts on 250 shares. Assuming everything is ATM initially, and we assume no time value on the options, that would be a “value” of 250 * $20 = $5,000 for the treasury. No risk. (Leaving aside the other 750 shares of stock I own.) Plus I owe $4,000 in embedded taxes. So that nets to long 750 shares of stock plus $1,000. (Which is the tax rate times the basis of the whole position.)

So when you buy a stock, it’s like owning one minus your tax bracket of it in a Roth (so 750 shares in this case) plus your tax bracket times the basis of dollars (no interest on this fixed income position; it’s like holding actual currency). So if I purchased, right now, 1,000 shares of the stock at $20 with a tax bracket of 25%; it’s like having $5,000 plus 750 shares of tax-free stock. That is much lower risk (beta) than the 1,000 shares of the stock in a Roth.

Eighteenth, there is a bill (separate from the big reconciliation tax bill) that would eliminate the advantage that ETFs have to use in-kind redemption mechanisms (“heartbeat trades”) to avoid capital gains taxes. If something like this ever passes, then it makes direct indexing much more attractive. See here and here for details. I agree with John Rekenthaler’s take.

Nineteenth, good post here on risk. I own, and have read, Reminiscences of a Stock Operator. People see extreme wealth from risk-taking and think that is the best path. But they don’t see the risk-taking that led to bankruptcy and penury. Survivorship bias!

Twentieth, there was a discussion on some financial industry message boards recently that led to a recommendation of The FairTax Book as a quick read. I thought my contribution (particularly the MMT portion) might be interesting to some of you folks:

I read the FairTax book a long time ago and it’s utterly unworkable. They cook the books on the rate to start with (this is from memory, so I may have the figures wrong), but I think they claim a 23% rate covers everything, but they compute the 23% by computing it on the price including the tax. In other words, it’s really X%/(1+X%)=23% and when you solve for X% that would be about 30%. The pitch is “abolish the IRS” and “people don’t cheat on sales taxes” but if you have a 30% rate people would try to evade those. People (mostly) don’t cheat on sales taxes because it isn’t that much money so why bother. And there would have to be some agency enforcing the tax collections which would become as hated as the IRS even if it has a different name.

Don’t get me wrong, I personally would love it – I don’t spend all that much of my income! It’s like an automatic unlimited Roth for everything you don’t spend!

The problem (IMHO) is the level of expenditure we are trying to finance is just difficult to do. Since no one wants to pay for what they want, we get (from Russell B. Long):

Don’t tax you,

Don’t tax me,

Tax that fellow behind the tree.

And crazy ideas like MMT.*

I’m a classical liberal (not a liberal). My pick for best small book to read is this one: The Law.

“The problem with socialism is that you eventually run out of other people’s money.” – Margaret Thatcher

*Here’s my aside on MMT for those interested. This is a very simple explanation that glosses over a little of the detail, but I don’t think misses anything essential. Assuming the global economy grows there is a need for more dollars (global, not domestic, because a lot of dollars are held elsewhere). Right now, to increase the money supply, the Fed buys treasurys. Those holdings of treasurys are basically permanent (unless the global economy shrinks at some point or the dollar is no longer used as much). The Fed uses the interest from those to pay its expenses and then remits the rest of the interest to the treasury. So if we think of this as a household, you find some money (the amount the Fed prints, which we will assume is exogenous) and redeem some debt (pay down your credit card) and then have the extra funds to spend (the interest is now less) on stuff. If you just spent the funds directly it isn’t different. (I.e. assuming the spending is the same, the level of credit card debt is eventually exactly the same. Just in one case you pretend to pay down your debt and then run it back up, where in the other you just spend it directly.) So, for MMT, if the level of money printing is held to the same level that the fed would have created with open market purchases it leads to the same place. I do worry that the MMT folks don’t realize that you are still constrained by the normal growth of the money supply or you will have higher inflation. The problem (again IMHO) is that “borrowing” to buy stuff feels/seems worse than “printing” to buy stuff. Since I think the problem is the expenditure level is too high, I don’t like anything that makes it easier to tax/borrow/spend even if it’s just a change in mental framing. I would love it if there was no withholding allowed, no sales taxes at POS, etc. Everyone should have to write a check every April 15th for their total contribution to the commonweal. That would lead to a very different level of expenditure and much better debates on taxes and spending! Withholding was originally Friedman’s idea but he wished it didn’t last.

Twenty-first, I was surprised that here “high net worth individuals” were defined as “a net worth over $1 million.” Seems pretty low to me but it’s only 12% or so of the population.

Twenty-second, don’t “buy the dip” rather buy all the time. Excellent analysis here.

Twenty-third, fantastic Reminiscences of a Strategist. I added a few of the quotes to my Ruminations by Other People (note she misattributes a few), and it’s another plug for Reminiscences of a Stock Operator which I mentioned above. I miss Wall Street Week with Louis Rukeyser, too.

Finally, my recurring reminders:

J.P. Morgan’s updated Guide to the Markets for this quarter is out and filled with great data as usual.

Morgan Housel and Larry Swedroe continue to publish valuable wisdom. Just a reminder to go to those links and read whatever catches your fancy since last quarter.

That’s it for this quarter. I hope some of the above was beneficial.

If you are receiving this email directly from me, you are on my list of Financial Professionals who have requested I share things that may be of interest. If you no longer wish to be on this list or have an associate who would like to be on the list, simply let me know.

We have clients nationwide; if you ever have an opportunity to send a potential client our way that would be greatly appreciated. We also have been hired by some of our fellow advisors as consultants to help where we can with their businesses. If you are interested in learning more about that arrangement, please let us know.

We also offer a monthly email newsletter, Financial Foundations, which is intended more for private clients and other non-financial-professionals who are interested. If you would like to be on that list as well, you may edit your preferences here.

Finally, if you have a colleague who would like to subscribe to this list, they may do so from that link as well.

Regards,

David

Disclosure

|